The Invest-Tech sector in India has witnessed remarkable growth in recent years, with a surge in innovative startups offering investment solutions. P2P lending platforms, offering diverse opportunities for both investors and borrowers, have also increased in recent times. 13 Karat is the latest entrant in this segment. In this 13Karat review, we will delve into its features, benefits, and how this platform works.

What is 13Karat?

13Karat is a Peer-to-Peer enabled lending platform that allows individuals in India to invest in Peer-to-Peer (P2P) lending opportunities offered by RBI-registered P2P NBFCs. This platform, owned by Sqrrl Fintech Pvt. Ltd provides the potential to earn returns of up to 13% per annum. The platform is accessible on mobile apps- Android & iOS and has more than 50000 downloads at the time of writing this article.

Company Behind 13Karat – Sqrrl Fintech Pvt. Ltd

13Karat is a part of Sqrrl Fintech Pvt. Ltd, a leading fin-tech company. Sqrrl was recently acquired by CASHe, one of India’s leading consumer credit providers, in an all-cash deal in the year 2022. Sqrrl Fintech also has another mobile app- Sqrrl which helps customers with mutual fund investments.

About CASHe

CASHe, one of India’s leading app-based personal credit providers, was established in April 2016. It is a strong player in the digital personal lending space in India being managed by professionals with several years of experience.

It offers loans ranging from Rs 1,000 to Rs 4,00,000 to young professionals, utilizing advanced technology and data analytics to assess creditworthiness through the Social Loan Quotient (SLQ) based on mobile and digital behavior.

They lend to salaried borrowers with a monthly income of 22K & above whose bureau score is 600+ OR the borrower is new to credit. They lend only to people working in MCA-registered companies and not in proprietorships. The loans are also, generally, short tenure (3/6/9 month) personal loans and also they offer “buy now pay later” and credit lines. This is similar to the lending profile of P2P companies and other NBFCs.

CASHe’s FY22 operating revenue witnessed an impressive 2.36-fold increase, soaring to Rs 247.91 crore from Rs 104.69 crore in FY21, as reported in its consolidated financial statements filed with the Registrar of Companies.

They have a whooping 3.5 Crore + downloads & have disbursed over 10000 Crores worth of credit to eligible borrowers over the years.

13Karat is a source of borrowing for Cashe. They are focussed on short-term lending hence the investment profile in 13karat is also 3 and 6 months.

How 13Karat Works?

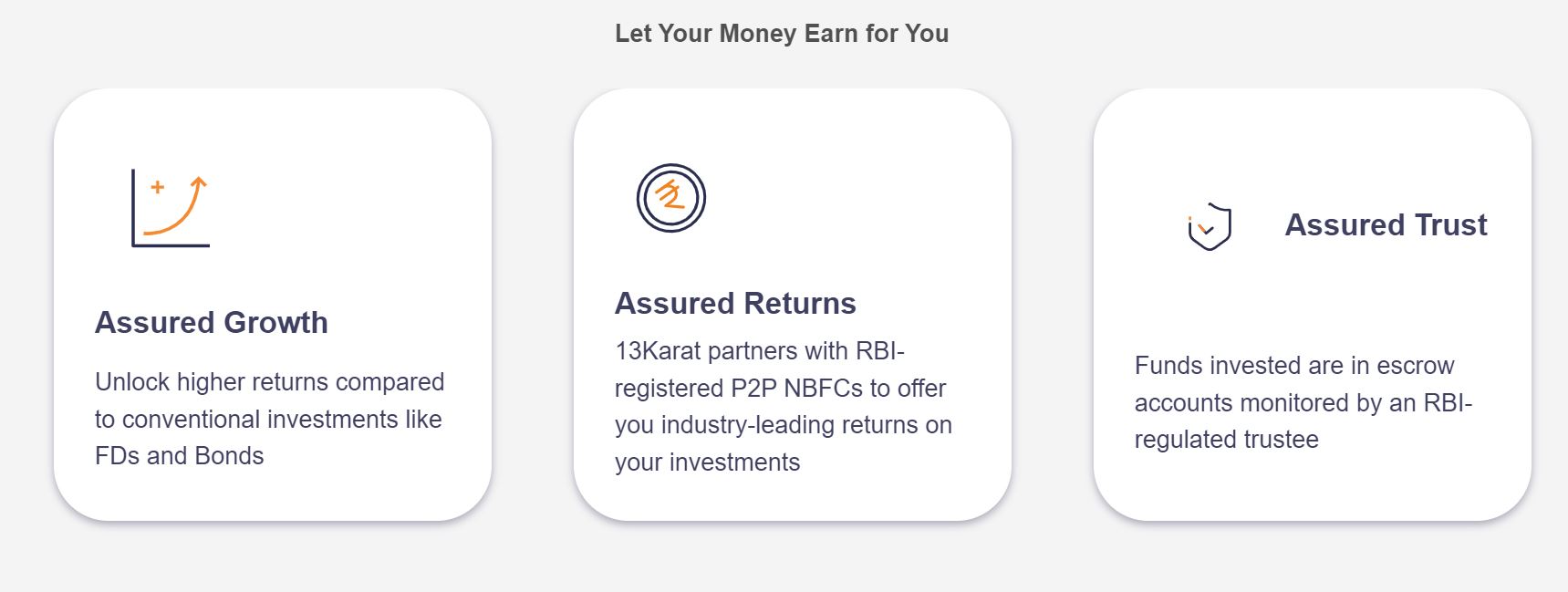

13Karat has forged agreements with RBI-registered P2P NBFCs- Lendbox, which has the necessary licenses for P2P lending. These partnerships allow management of the funds deposited by the investors. Through this partnership, the invested amount finds its way into a diversified pool of credit-worthy borrowers, sourced by the Cashe. This approach mitigates risk and diversifies investments, providing investors with a prudent and secure way to grow their wealth.

Investment Options in 13Karat App

13Karat offers two investment options for its investors:

| Plan | Lock In | Interest |

| 13K | 6 Months | Up to 13% p.a |

| 12K | 3 Months | Up to 12% p.a |

13k

With this option, investors can commit their funds for a fixed tenure of 6 months and potentially earn interest of up to 13% per annum. Please note that the investment is locked in for the entire 6-month duration, and premature withdrawal is not possible.

12K

This option allows investors to invest funds for a fixed tenure of 3 months, with the potential to earn interest of up to 12% per annum. Investments are locked in for the entire 3-month duration. Similar to the 13K option, early withdrawal is not permitted.

Key Features of 13Karat

Following are some of the key features of the 13Karat app.

- Start Small or Go Big

Investors have the flexibility to start with a small amount, as little as Rs. 500, or go as high as Rs. 50 lakhs. Whether you’re just beginning to invest or are looking for a substantial opportunity, 13Karat accommodates your preferences.

- Auto Roll Over

Seamlessly reinvest your money at maturity by opting for automatic rollover. This feature simplifies the process and ensures that your investments continue to work for you.

- No Investment Fee

There are no hidden charges or investment fees, allowing you to make informed investment decisions without incurring additional costs.

- Monthly Interest Payouts

Interests are added on a monthly basis to your deposits, and they are available for withdrawal at maturity based on the chosen investment plan. This regular interest payment can provide you with added financial flexibility.

- Quick Bank Deposit

Upon maturity, the principal amount along with the interest earned on your investment through 13Karat will be deposited into your bank account by default on T+4 working days. This quick deposit process ensures that you have easy access to your funds when needed.

- Zero Charges

As part of its commitment to transparency, 13Karat does not charge any fees for depositing or withdrawing your funds. This approach simplifies the investment process and ensures that you can maximize your returns without worrying about hidden costs.

How to Register and Start Investing with 13Karat

Getting started with 13Karat is a straightforward process, and you can begin your investment journey in a few simple steps:

CLICK HERE to download the app & start investing in 13Karat. You can also use the QR code to directly download the app.

- Eligibility: To invest through 13Karat, you need to be 18 years or older, and you can be either a resident or non-resident of India. You must have an active PAN card and an Indian bank account. NRIs can also invest through their NRO bank account.

- Complete KYC: To begin investing, complete the PAN and Aadhar-based KYC process. This is essential to confirm your identity and comply with regulations.

- Bank Account Verification: You’ll need to provide your bank account details for verification. This step ensures that the name on your bank account matches the information provided during KYC. Your privacy is valued, and this information is used solely to facilitate your investment.

- Select Your Investment Option: Choose between the 13K or 12K investment plans, depending on your investment goals and preferences. You can start with as little as Rs. 500.

- Make Payments: You can make payments via UPI and Net banking. Please note that credit card payments are not allowed for P2P investments, in adherence to RBI regulations.

- Enjoy Monthly Interest Payouts: With 13Karat, you receive monthly interest payouts on your deposits, and these earnings are available for withdrawal at maturity.

- Withdraw Your Funds: Upon maturity, the principal amount along with the interest earned on your investment is deposited directly into your bank account, ensuring a quick and efficient process. If you prefer to reinvest, the auto-invest option is available on the 13Karat platform.

13Karat Alternatives

Some of the other alternatives in the market which follow a similar model are as follows:

Per Annum from Lendbox: Lendbox, one of 13Karat’s NBFC partners, has similar offerings directly with the name- Per Annum. The rates of interest offered are slightly lower than 13k. However, the minimum lock-in is lower than 13K.

Liqiloans: One of the most popular platforms in this segment. The interest offered varies according to the plans, however, it is lower compared to 13Karat’s rates.

Indiap2p– It does not provide instant liquidity but has a high-interest rate up to 18% per annum.

Conclusion

In this 13Karat review, we’ve explored the features and benefits of the platform. If P2P platforms have an asset allocation assigned to your portfolio, you can reduce the risk further by diversifying across multiple P2P platforms- 13Karat being the latest addition.

The tech- UI/UX definitely needs a major upgrade. The UI is not the best in class and the app is buggy- encountering a lot of issues on multiple devices we tested.

The backing of a decently strong fintech player along with high interest rates in the segment makes it a strong contender. However, as always, make sure you do due diligence at your end before committing money on any platform.

We will be investing a small amount and sharing our monthly performance of the investments.

Frequently Asked Questions (FAQs)

What is 13Karat?

13Karat is an Invest-Tech platform that allows individuals in India to invest in Peer-to-Peer lending opportunities offered by RBI-registered P2P NBFCs.

Who owns 13Karat?

13Karat is owned by Sqrrl Fintech Pvt. Ltd, a prominent player in the financial technology sector.

How does 13Karat work?

13Karat partners with RBI-registered P2P NBFCs to deploy investors’ funds in a diversified pool of carefully selected borrowers, following RBI regulations.

What are the investment options in 13Karat?

13Karat offers two investment options: 13K (6-month tenure) and 12K (3-month tenure), with potential returns of up to 13% and 12% per annum, respectively.

How can I start investing with 13Karat?

To start investing, you need to be 18 or older with an active PAN card and an Indian bank account. Complete the KYC process, select your investment option, make payments via UPI or Net banking, and enjoy monthly interest payouts.

What are customer 13Karat Reviews?

Overall, customer 13Karat reviews seem to be positive. The app has around 118 reviews at the time of writing the reviews on Google Playstore and the average rating is 3.8 stars out of 5. Most of the users are having issues with tech or UX.

These FAQs provide answers to common queries about 13Karat and its investment process. It’s important to explore further details and conduct due diligence before making investment decisions.

its same as mobikwik

mobikwik also have collaboration with Landbox and providing 12.99 for 3 months Lock in.

so both are same but mobikwik has lower Lock in period.

Hi Hardik,

The difference is that mobikwik lending is done for mobikwik borrower base while 13k to cashe . I find cashe has better borrower profile(salaried people with short term requirement) and NPA performance of NBFC is available online .