For years, Indian investors mostly relied on traditional investment options like Fixed Deposits, Mutual Funds, Stocks, PPF, Gold, and Real Estate. While these options are still very popular, many investors- especially young investors are looking beyond the usual choices. This is where alternative investments come into the picture.

In this article, we will cover the different types of alternative investment options available in India, popular platforms offering these investments, a monthly model portfolio for ₹25,000 & important risks and factors to consider before investing.

What are Alternative Investments?

Alternative investments are investment options that do not fall under traditional categories like stocks, bonds, or bank deposits. They usually offer higher returns compared to traditional investments, in many cases with higher risk & allow greater diversification. Earlier, many of these investments were available only to wealthy investors or institutions. However, today, many fintech platforms have made them accessible even for retail investors in India.

Alternative investments also have low correlation with the stock market. This means when equity markets fall, your invoice discounting deal or bond NCD is largely unaffected — it follows its own credit cycle, not Sensex movements. This makes alt investments a genuine diversifier, not just a higher-yield FD substitute.

Types of Alternative Investments Available in India

Following are some of the popular Alternative Investments Available in India

1. Invoice Discounting

Businesses often raise invoices but get paid only after the credit period is over- typically upto 90 days. Invoice discounting lets investors fund these unpaid invoices in exchange for a return when the invoice is settled. It is a short-tenure investment option, usually varies from 30 to 90 days, and yields 9 to 13% p.a.

Platforms: Grip Invest, Amplio, Altgraaf, Ultra Club by Tapinvest

2. Bonds and NCDs

Non-Convertible Debentures (NCDs) and corporate bonds are fixed-income instruments issued by companies. They pay regular interest and return the principal at maturity. They are SEBI-regulated and relatively stable.

Platforms: WintWealth, Aspero, Golden Pi, BondScanner, Altifi

3. P2P Lending

Peer-to-peer lending connects investors directly with borrowers. You earn interest as the borrower repays. Returns are higher than FDs, but default risk is real. Once a favorite category among alternative investment enthusiasts in India but no longer much popular, having many platforms pivoted to other models.

Platforms: IndiaP2P, Lendbox, I2IFunding

4. Fractional Real Estate

Own a fraction of a commercial or residential property without having to shell out lakhs & crores for buying property single handedly. You earn rental income and potential capital appreciation.

Platforms: Per Annum, Alt DRX

5. Insurance Policy Assignment

A unique niche: you purchase existing life insurance policies from original holders at a discount and earn returns when the policy matures. Returns can be as high as 15% which are tax-free under Section 10(10D) in most cases.

Platform: Policy Exchange

Before You Invest: 4 Non-Negotiables

Alternative investments are not for everyone. In fact, most retail investors should be fine with traditional investment options like Fixed Deposits, Mutual Funds, Stocks, PPF, Gold, etc. Before allocating a single rupee, make sure:

- You have 3–6 months of emergency fund in liquid instruments (savings account, liquid fund)

- You already invest significantly in traditional investment instruments like Fixed Deposits, Mutual Funds, Stocks, PPF, Gold, etc. — alt investments are a complement, not a replacement

- You are comfortable with lock-in periods and the possibility of delayed or missed payments or defaults

- You have done exhaustive research about the platform & the instrument before investing

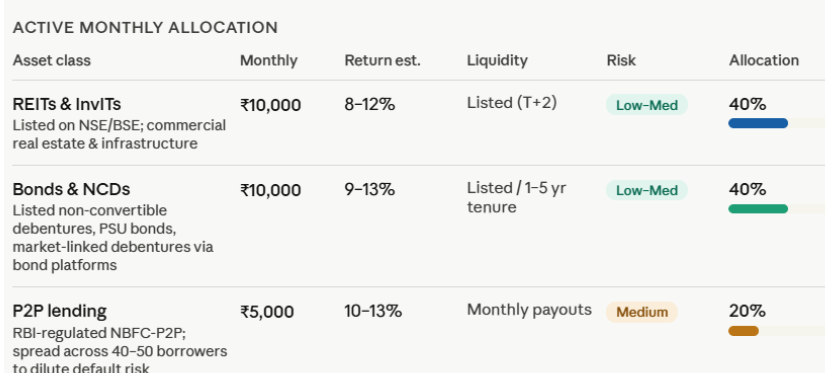

Model Portfolio: How to Invest ₹25,000/Month in Alternative Investments

Here is a sample monthly allocation across four asset classes. Since many investment options have a high minimum investment (in many cases upwards of Rs.25000 or 50000)- have considered only those options where investing smaller sums are possible.

- REITs & InvITs: ₹10,000 (40%)

- Bonds & NCDs: ₹10,000 (40%)

- P2P lending: ₹5,000 (20%)

For invoice discounting, you’ll have to follow a periodic deployment strategy. Park ₹5,000/month in a liquid mutual fund. Deploy ₹50,000 every ~2 months into invoice discounting (30–90 day trade receivables). Capital recycles quickly and re-parks until the next deployment window.

Conclusion

Alternative investments are becoming increasingly popular & accessible for retail investors in India. Today, even investors with ₹25,000 per month can build a diversified portfolio across bonds, invoice discounting, P2P lending, etc..

The biggest advantage of alternative assets is higher yields. They can complement traditional investments and potentially improve overall portfolio stability and returns. However, investors must understand that higher returns often come with higher risks.

The best approach is to start slowly, diversify properly, and focus on long-term wealth creation instead of chasing unrealistic returns. With disciplined investing and careful platform selection, alternative investments can become a valuable part of your financial journey.