When it comes to investing in P2P platforms I have covered various aspects related to calculation of returns and factoring of defaults .One important factor in choosing a platform and duration loan I would want to add is Platform fees!

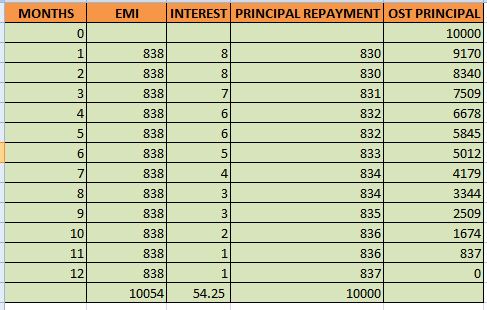

How is the Fees calculated? Each platform has its own method of levying the charges.Some of them charge an upfront fees while other charge on the EMI. It is basically comparison of a flat interest rate vs reducing balance interest rate.How does this impact us? Here is comparison between 1% Fees charged upfront on 10000 investment vs 1% charged on ROI. Paying on total principal is more expensive for shorter tenors.

We have taken a 12 month loan with 1% fees deduced from ROI. We end up paying 54.25 versus 100 if we would have paid upfront. Paying upfront is better deal when tenor is longer as your cost is spread across time.

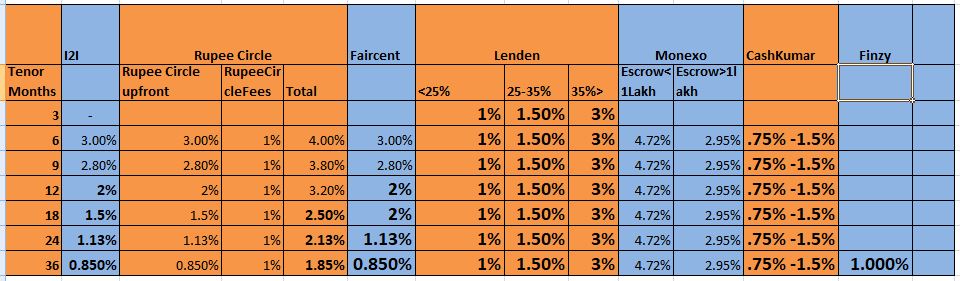

Here are the Fees details of the most popular platforms:

- I2I Funding: Charge 1% upfront plus gst . If you want to compare it with ROI based charges ,for 1 year it is equivalent to 2% deducted from ROI and 1.13% for 2 years. So longer tenor loans are better in I2I Funding.

- Faircent: Same as I2I funding though it has higher registration charges also.

- LendenClub : It has ROI based fees. Fees is variable depending on which ROI category we are investing. For Loans below 25% you have to pay 1% while for 48% you end up paying 3%. As it is a ROI based fees tenor does not impact fees .Ideal for short duration loans

- RupeeCircle: Charge 1% with each EMI similar to Lenden. One issue is they charge 50 Rs document handling fees .For disbursement size of 5000 it is equivalent to1% which makes the platform expensive for short term loans. Only beyond 18 months its feasible to invest in the platform at decent cost.

- Cashkumar :ROI based fees which varies from 0.75% to 1.5%. One of the cheapest platform and ideal for short duration.

- Monexo: For Investment less than 1Lakh in escrow they charge 4% +gst = 4.72% from ROI which is a bummer!

- Finzy :Only have 36 months loan and they charge 1% from ROI which is slightly more than I2I for equivalent tenor.

Below is a reference table where we can compare platform fees for various tenor .I have converted all Fees in ROI based fees.

It means all numbers are average annual interest you have to pay from your ROI if you invest in that platform in that tenor.

eg: FOR I2I in 18 month loan you pay 1.5%per annum of your ROI as fees while in 24 months you pay 1.13%.

I have highlighted the tenors for each loan where you should invest .In short this is how your platform and tenor combination should be:

0- 18 months : LendenClub and Cashkumar

18- 36 Months: For 23% and less ROI loans prefer I2I,For 23% plus loans go for RupeeCircle,As a rule longer the duration of loan safer the borrower I prefer.

Offcourse you can use LendenClub and Cashkumar for longer term loans also but its best to stay diversified.

Happy Investing!

Hi Rohan!

Your in-depth analysis is very helpful (though I can’t claim I understand all of it).

When you say:

“18- 36 Months: For 23% and less ROI loans prefer I2I,For 23% plus loans go for RupeeCircle…”

Do you mean 23% is effective ROI (on reducing balance) or is it nominal ROI (which actually becomes less if you consider reducing balance)?

Also, Lendbox charges only an upfront registration fees of Rs.500. There are no other deductions till your invested amount crosses Rs.1 lac. Could Lendbox be a better option than the ones you have compared in your post?

A detailed analysis of Lendbox would be of help.

Regards,

Bhadresh

Hi bhadresh,

The interest rate given in all P2P platform are always nominal ROI ,the same which we have in home loans. If you do not reinvest then your effective ROI will be lower.Why I have put I2I ,Rupeecircle and Lenden in different category is due to how they charge fees.I2I charge upfront fees (fixed) for each loan. It means if we have long dated loan you end up paying low effective fees while Lenden charges effective Fee which makes it independent of duration.

Rupee circle is a combination( fixed + effective fee) so it falls somewhere in between.

Lendbox I had tried long time back. 2 major red flags I had observed where. Minimum investment 10k is tad too high for a small portfolio.

Reviews were not good and they dint display platform performance .

You need to be confident on the promoters also and I dont have much knowledge about them

Thank you!

Hi Rohan,

Thanks for your great work on the P2P area which is still surprisingly not popular in India.

Today, I have opened an account in RupeeCircle using your referral code PIND145

I always had this confusion between ”effective ROI” and ”nominal ROI”. Many new investors are allured towards P2P on seeing the high nominal ROI but infact realise this is possible only when reinvested properly within the stipulated interest period.

Could you please write a blog post explaining the differences between the ”effective ROI” and ”nominal ROI” and also what is the ROI if we do not reinvest or if we reinvest on a longer duration loan or if we partially reinvest ?

Also in my opinion, a true comparison of the interest rate with traditional investment options should consider the effective ROI where we do not mostly reinvest since we are basically saving to achieve our financial goal at a certain period of time.

Hi Balaji,

P2P loan is different from traditional investment in the sense that your investment is amortised during the life of the loan. It would be unfair to compare it to say a FD without reinvesting because in 1 Year FD at 8% you get 8Rs on 100 after a year and 100 at end. In P2P you get around 9rs every month which sums to 108 in 1 months (apprx). If you are not reinvesting then most of your capital is earning 0%. That’s why best way to calculate return is XIRR( internal rate of return) which factors in the cash drag(not reinvesting impact ) also and then you can benchmark it with any investment. All my numbers are XIRR . I had published methodology too.

https://www.investopedia.com/terms/i/irr.asp