There are 2 Kind of people :

- Who believe you can’t time the market

- Who believe you should invest in market only when it’s undervalued.

Both are correct to an extent , though it’s not impossible to time market but to do it consistently is impossible but it is possible to improve your odds of gaining higher returns if you increase your asset allocation when it is undervalued and slightly reduce it when it’s overvalued.

Again people will argue that’s its inefficient because you have to sit on cash which doesn’t yield much but that opinion is based on the assumption that other asset classes do not give similar yields like Stock.

Why a Diversified Portfolio is important?

Assets which have low correlation with each other don’t move together ,it means when an asset value drops the other asset won’t drop that much and vice versa

Is it possible to create a portfolio which has multiple assets which have low correlation yet overall high yield of portfolio . Let’s try doing that.

First we need to address the market factors which affect my assets:

- Equity Price

- Real Estate

- Interest Rate

- Currency Rate

- Credit Risk

- Retail Credit Risk

Our model Portfolio should cover three important factors:

- Ensure Assets have low correlation

- Portfolio Liquidity Matches our Requirement

- Asset Allocation is in tandem with our market view and Risk appetite.

- Assets have low correlation:

I have considered the asset classes provided in the table:

* REIT were launched recently, I have annualised the returns achieved till date

All the assets in Green have practically zero correlation with any asset class and have almost zero risk.

I have already covered how we can create an Insured FD risk less portfolio.

http://randomdimes.com/2019/create-a-risk-free-fixed-deposit-portfolio/

EPF is sovereign debt. Arbitrage funds invest in cash/future arbitrage hence no credit risk.

So 31% of my portfolio is risk free and has a yield close to 8.2%.

Now I have to check correlation of 69% portfolio:

Equity with P2P lending Correlation:

For my own portfolio P2P and equity has not shown much relation as P2P returns have been consistent while equity had been volatile during the period. Historically let’s see how was the correlation.Based on the reports of 2008 Crisis P2P lending gave positive returns in that year.Well in future the draw down may be higher but still the correlation to equity has been low.

Equity vs REIT: Equity and REIT have historically low correlation and even during the 2008 mortgage crisis correlation never reached one.

Similar studies have shown how gold and Equity can have negative correlation during crisis and give a portfolio boost during crisis

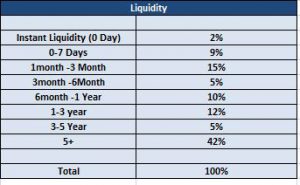

- Portfolio Liquidity Matches our Requirement

If you invest in a portfolio without liquidity in mind you might have to unwind the portfolio at the wrong time which can really ruin your investment strategy. It is prudent to have ball park figure of liquidity.

People who want immediate liquidity should allocate more to Arbitrage Fund, Short dated P2P etc.

- Asset Allocation is in tandem with our market view and Risk appetite.

We have achieved 2 things by having this diversified portfolio compared to only equity portfolio.

Advantage 1:

Our asset classes : FD , P2P , arbitrage funds have lowered the volatility which an equity only portfolio faces.

Almost 50% portfolio has close to zero volatility.

Advantage : You don’t lose your everyday sleep because of 5-6% drop in portfolio.

Advantage 2:

Though our portfolio is less volatile does not mean it is free from black swan events like 2008 Crisis or impact of market risk factors.

What is good about this portfolio we can play market risk factors to our advantage :

How?

We know currently rupee has strengthened , Interest Rate has gone down and Credit spread has gone up.

I have made my portfolio exposure higher in US equity, Credit Funds and short dated funds. When these factors reverse I will book profit and transfer it to Long Dated Bonds etc.

We know certain things follow cycle :

Interest Rate

Currency

Equity

We cant time them but we can increase our weightage based on the fact that which end of spectrum they are. If Equity valuation is over the top I will allocate more to other asset classes.

At any time I have sufficient capital in other asset classes to transfer to an asset which has become cheap.

Even in case of a black swan event unlike a pure equity portfolio my draw down would be less in some asset classes , like insured FD, arbitrage etc.

Additional Feature: I have put my long term holding as collateral and used that to get derivative trading margin. I am able to create conservative short position to balance some of my long portfolio and also earn some yield in flat market. Offcourse this requires to have good understanding of option trading and should be implemented by those who understand the nuisances of options.

In my table I have prepared a column for my target return for each asset class and next to it I have put the actual 1 year performance. Total returns are published.

I will update the portfolio monthly with rebalances if any

Conclusion: You can create a balanced portfolio which can give similar returns as an all equity portfolio with less volatility.