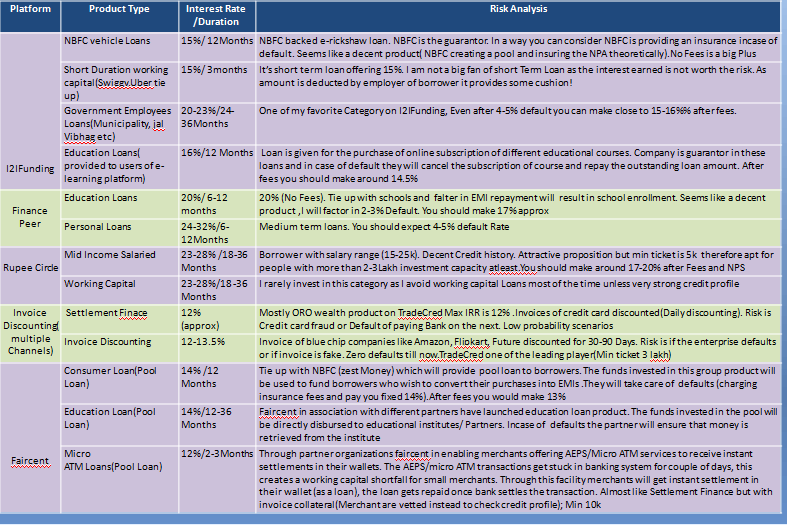

This month I have added a new product available on Faircent. The new pool loans seems to be a good proposition and I thought I will give it a try . I would be investing only in pool loans in Faircent. Before I publish my performance I am briefly reviewing the some interesting loans available on various platforms with brief analysis

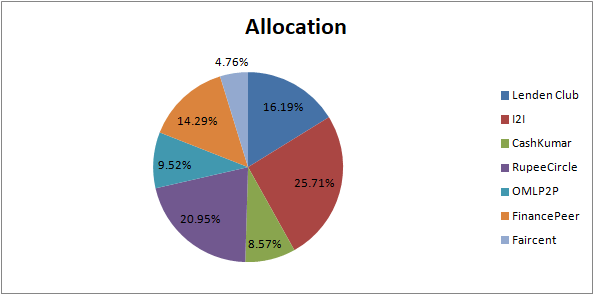

Portfolio Composition for October

Portfolio Changes:

- Primarily sticking to the 3 platforms like last month: I2IFunding , RupeeCircle and FinancePeer.(Good quality loans, high volume of loans)

- I am only reinvesting EMI in these 3: LendenClub, OMLP2P and Cashkumar. Primary reason is that number of borrowers are too few to invest more money

- Faircent has recently started few pool loan product where I have started investing recently .

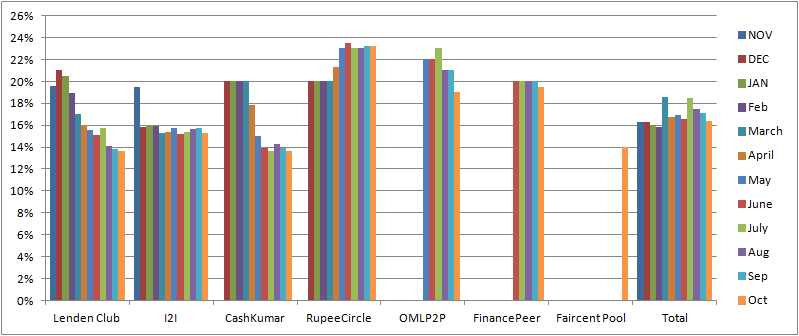

Portfolio Performance

Performance Analysis:

Key Points from this month’s performance are:

- LendenClub: I have decided to totally discontinue Insta loan. Reason is that the interest I get is around 40 bucks in 3 months for 500 investment in InstaLoans. Even if 1 out of 13 default(7.7%) I am in loss, this makes it very sensitive to the underwriting and instaloans by nature are risky. I will continue to reinvest in long dated loans with preference to existing borrower

- I2IFunding : I2Ifunding performance seems to be good but one thing I noted was that loans backed by NBFC(15%) are almost as good as my portfolio return(Approx 15%). It means I did not generate extra return by active management(I could have just invested in NBFC backed loans). If I see the granular performance I realise most of my defaults are in my early investments( working capital loans, High Ticket size etc) . Platform underwriting has improved over time and also my own skills.In next 6 months I expect my yield to rise by 1% approximately

- RupeeCircle :Great performance continues. One loan is in 40 days delay so I have booked 50%of the outstanding principal as NPA as conservative measure. I am concentrating on people with decent salary, High account balance and low EMI to salary ratio

- FinancePeer : Education Loan investment has been pretty successful with zero defaults till now.Interestingly they have tie up with institutes which will refund money in certain cases of borrower defaults

- OMLP2P : The performance is good but with only 1-2 loans in a week I dont see much investment opportunity as of now

- Cashkumar: Same problem.Not many loans and they disappear really fast. Cash lying idle!

- Faircent Pool Loans

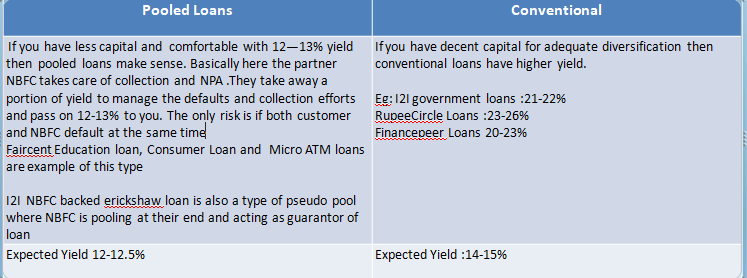

Faircent has recently started some pool Loans .Advantage of pool loan is that it provides instant diversification and is great for people who are starting(it’s like the ETF of p2p loans) ,have less capital,or who don’t have much time for due dilligence.

3 categories seem interesting

- Consumer Loan

- Education Loans

- Micro ATM loans

Consumer Loans:

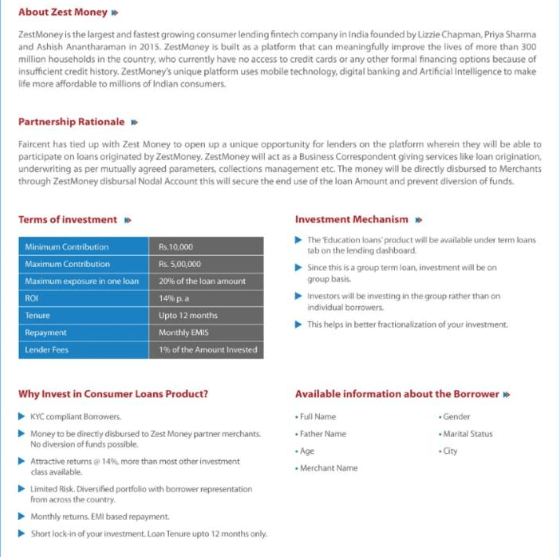

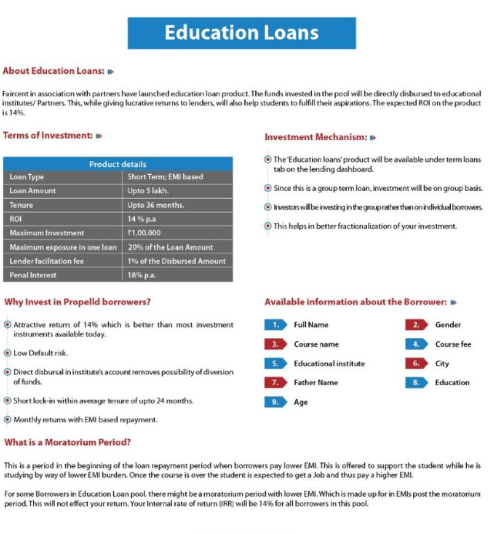

Tie up with NBFC (zest Money) which will provide pool loan to borrowers for items they bought from their partners The funds invested in this group product will be used to fund borrowers who wish to convert their purchases into EMIs .They will take care of defaults (in a way charging insurance fees and pay you fixed 14%).After fees you would make 13%

MicroATM Loans:

Through partner organizations faircent in enabling merchants offering AEPS/Micro ATM services to receive instant settlements in their wallets. The AEPS/micro ATM transactions get stuck in banking system for couple of days, this creates a working capital shortfall for small merchants. Through this facility merchants will get instant settlement in their wallet (as a loan), the loan gets repaid once bank settles the transaction. Almost like Settlement Finance but without invoice collateral(Merchant are vetted instead to check credit profile).The tie up is with a payment aggregator called Oxigen

Minimum amount is 10k and you should expect 12% fixed. It’s good alternative for people who can’t invest 50k in settlement Finance

Education Loan:Faircent in association with different partners have launched education loan product. The funds invested in the pool will be directly disbursed to educational institutes/ Partners. Incase of defaults the partner will ensure that money is retrieved from the institute .They will pass on 14% interest rate taking care of defaults

Pool Loan vs Conventional Loans

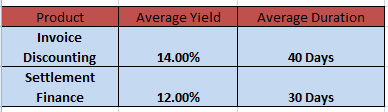

Invoice Discounting and Settlement Finance Performance:

I keep rolling my invoice discount investments. Invoices Invested till now

- Amazon

- Flipkart

- Future Enterprise

- Paytm

I have also invested in Settlement Finance which has daily settlement against Aadhar ATM invoice using TradeCred.

While In Invoice Discounting I invest in short duration invoices of Bluechip companies, in settlement Finance credit card or Aadhar Payment invoice which is paid T+1 day is financed for a day hence it’s an ultra short invoicing.

My current Portfolio yield and duration:

My Yield has gone up during the diwali week as lot of vendors were providing high interest rates to avail loans due to rising sales during diwali week which require more working capital

Footnote:

For alternate investment you can use these links

(First Use the link to register then add the Code “discount50@i2i” while paying to get 50% off)

Rupee Circle Referral Code- PIND145

Rupee Circle

LendenClub Referral Code – LDC11989

LendenClub

OMLP2P Referral Link

(Use Code MNJ6547)

Invoice Discounting Platform TradeCred Link:

https://buy.tradecred.com/onboarding/apply-now/TC0152

For other Invoice discounting platform ping me on 9967974993 or mail me on rohanrautela9@gmail.com

Why is Kredx missing? Have you stopped using it?

I have divided into both the platform so publish the aggregated number.

i2ifunding

1. short term loan (swiggy uber tieup) in i2ifunding is 12% for 45 days or am i missing something?

2. nbfc vehicle loans : fees are charged as regular loans only loans below 6 months are free

3. please review Group loans 25%

what are the registration fees for Faircent ?

my bad. yes 12% . Dont think that’s a good category to invest though. I2I loan against invoice is like settlement finance and yields 12% which seems better!