Indian investors are slowly moving beyond traditional savings instruments like fixed deposits & mutual funds. Earlier, investing in bonds was mostly limited to institutions and high net worth individuals. However, due to multiple fintech platforms offering these instruments & influencers raising awareness, instruments like corporate bonds and NCDs are gaining a lot of attention from retail investors.

Bonds offering high yields- 12 to 14% annual returns are attracting a lot of attention. Compared to bank FDs offering 6% to 7%, these returns look extremely attractive. Many investors see them as a way to generate better passive income. However, one needs to know why these bonds are available at such high yields & carefully take a call to invest in these depending on various factors.

In this article, we will understand whether high yield bonds are too risky and how investors can evaluate high-yield bonds properly before investing.

Why do Some Bonds Offer Returns as High as 14%?

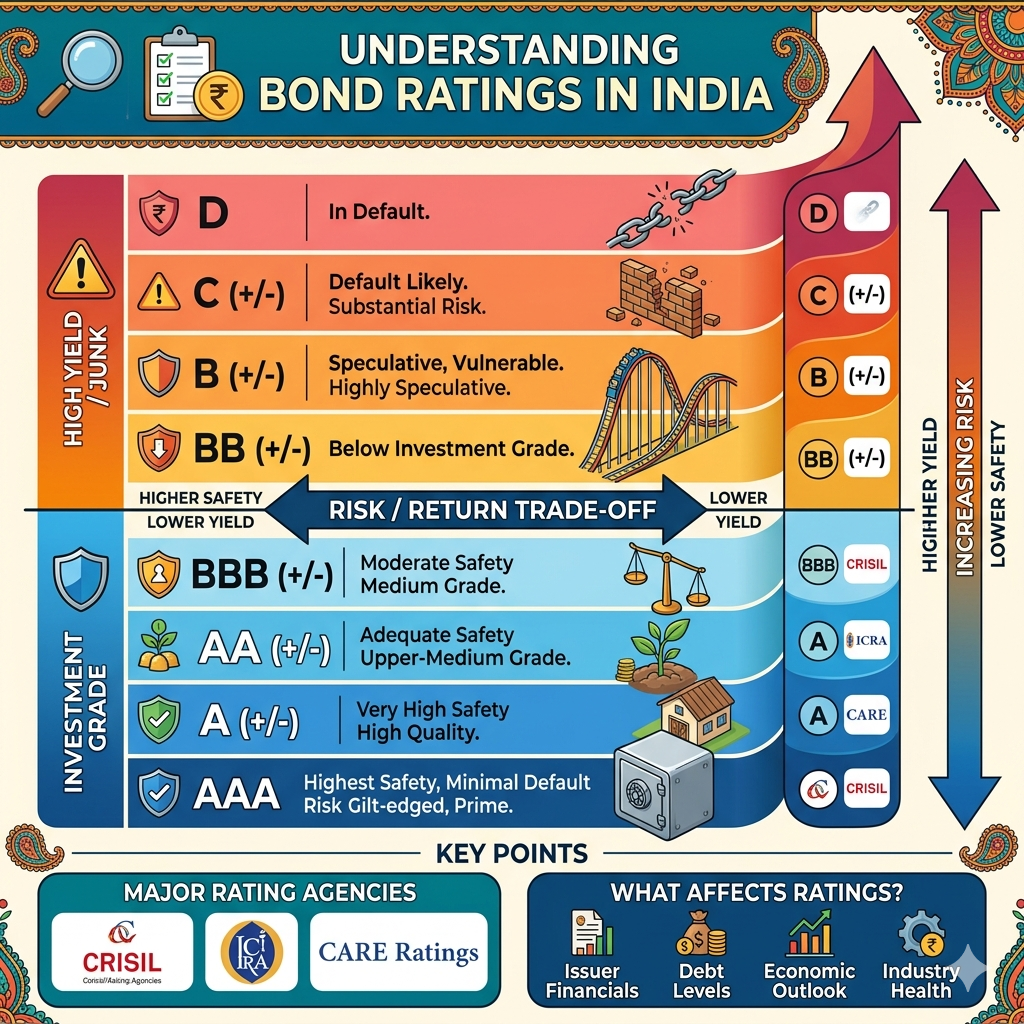

Companies usually offer high interest rates on their bonds when they cannot borrow money easily at lower rates. Safer companies can raise funds at lower interest costs. Riskier companies need to offer higher returns to attract investors.

This is why government bonds and highly rated corporate bonds usually offer lower yields (around 5-6% in current times). On the other hand, companies with riskier financial profiles may offer 12% to 14% returns. The extra return is basically compensation for higher risk.

Credit ratings also play a major role in bond pricing. Companies with strong ratings like AAA are considered safer. Lower-rated companies usually need to offer higher yields to attract investors. Rating agencies like CRISIL, ICRA, and CARE Ratings issue ratings to the bond issuing companies- which help evaluate the repayment ability of issuers. Lower ratings generally indicate higher credit risk.

Sometimes companies offering very high returns may already be facing financial stress. They may be borrowing money to repay older loans or manage liquidity issues. In such cases, repayment risk can increase significantly.

This does not mean every 14% bond is bad. Some companies may genuinely offer higher yields due to business expansion or market conditions. Also, having a riskier financial profile does not mean that the company will default your money. However, investors should do their research & understand why the company is paying such high interest.

How to Evaluate High-Yield Bonds in India?

- Credit Rating – Always check the credit rating before investing in any high-yield bond. Lower-rated bonds usually offer higher returns because they carry higher repayment risk.

- Purpose of Borrowing– Understand why the company is raising money. Borrowing for business expansion is generally better than borrowing to repay old debt or manage cash shortages.

- Company Financials- Check the company’s revenue, profits, debt levels, and cash flow. Weak financials or rising debt can increase the chances of default.

- Secured vs Unsecured Bonds– Secured bonds are backed by company assets, which may improve recovery chances during default. Unsecured bonds are usually riskier.

- Repayment History– Look at the company’s past repayment record. Frequent delays in interest or principal payments can be a major warning sign.

- Debt Burden– Companies with excessive debt may struggle during economic slowdowns. Lower debt levels generally indicate better financial stability.

- Liquidity of the Bond– Some corporate bonds are difficult to sell before maturity. Investors should be prepared to hold the bond till maturity if needed.

- Bond Tenure– Longer-duration bonds carry higher uncertainty because business conditions can change over time. Shorter tenures may sometimes reduce risk.

- Diversification– Avoid investing all your money in one high-yield bond. Diversifying across multiple issuers and sectors helps reduce overall portfolio risk.

- Offer Document– Read the bond offer document carefully before investing. It contains important details about risks, repayment terms, and security structure.

High-Yield Bonds vs Fixed Deposits

Most investors have the tendency to directly compare high-yield bonds with fixed deposits. Both generate fixed income, but their risk profiles are very different. Bank FDs offer lower returns because the risk is lower. Corporate bonds offering 14% returns carry significantly higher credit risk. Investors should understand this difference clearly.

Fixed deposits are generally much much safer than corporate bonds- especially the ones by public & private sector banks which are covered by DICGC- that insures bank deposits up to 5 lakhs per depositor per bank (principal + interest)

High-yield bonds can face repayment delays or even defaults. However, FDs are considered relatively stable investments. This is why you should never consider high-yield bonds to replace emergency funds or a major part of your savings- just going by the headline 12-14% returns.

At the same time, high-yield bonds can play a useful role in a diversified portfolio. Investors who understand risk may allocate a small portion to such investments. The key is maintaining proper balance.

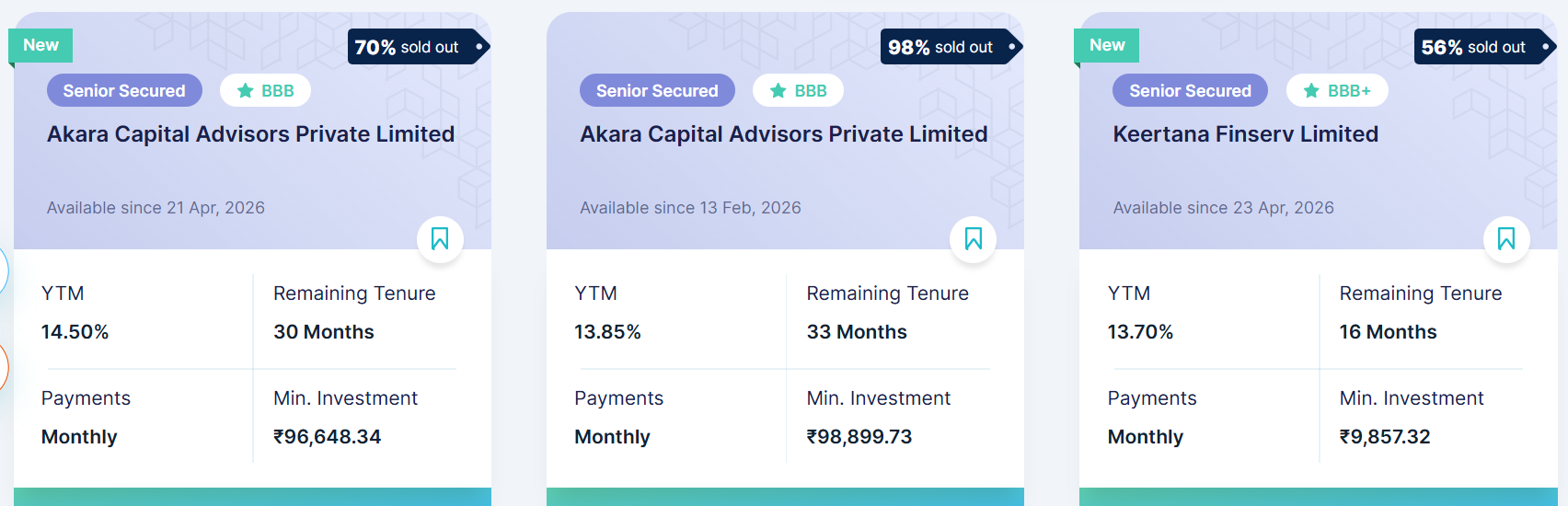

Platforms to Find High-Yield Bonds

Below are some platforms where you can look for high-yield bonds. Always compare yields for the bonds you choose on the platforms.

- Altifi

- BondScanner

- Aspero

- Goldenpi

- Grip Invest

- The Fixed Income

Conclusion

As mentioned in this article, high-yield bonds offering 14% returns are becoming increasingly popular among Indian investors. However, investors should remember the golden rule that high returns rarely come without higher risk.

Before investing in high-yield bonds, investors should check the company’s financial strength, business model, credit rating, and repayment ability.

High-yield bonds are not necessarily bad investments. When used carefully and in limited allocation, they can improve portfolio income. But investors should only invest after properly understanding the risks involved.

The smartest investors are not the ones chasing the highest returns. They are the ones who understand the balance between risk and reward before investing their hard-earned money.