As the financial year ends on 31 March 2026, most investors focus on tax-saving investments like ELSS or insurance. However, one of the most powerful yet underused strategies is tax loss harvesting.

Done correctly, tax harvesting can:

• Reduce your current year tax liability

• Improve long-term portfolio returns

• Help rebalance your investments

• Enhance after-tax compounding over time

Importantly, this strategy is not limited to stocks — it can be effectively done using mutual funds and ETFs as well.

This guide explains tax harvesting in simple terms, Indian tax rules, real impact examples, calculator framework, and practical switching ideas.

What is Tax Loss Harvesting

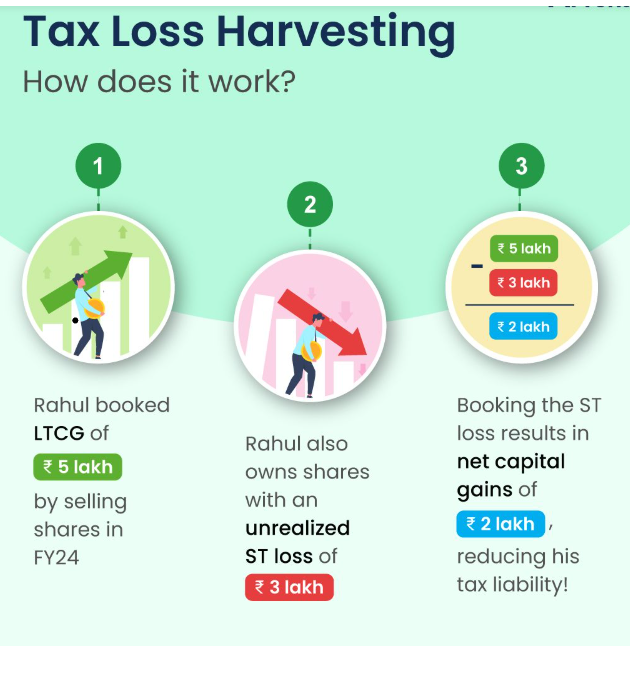

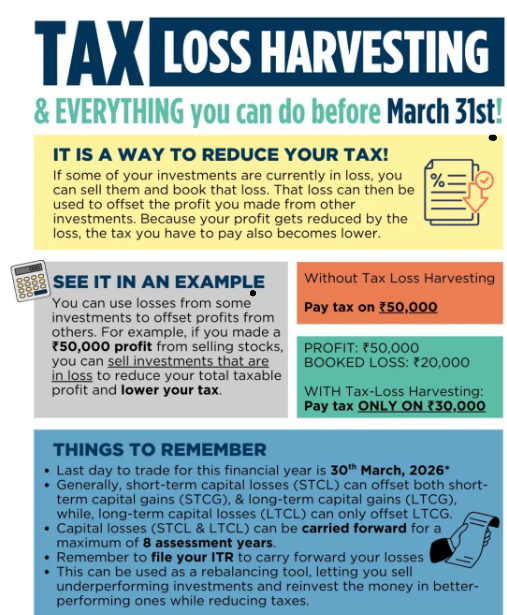

Tax loss harvesting means selling investments that are currently at a loss to offset gains you have already realised during the financial year.

Example:

- Profit booked in stocks = ₹2,50,000

- Loss in mutual funds = ₹1,00,000

Taxable gain becomes:

₹1,50,000 instead of ₹2,50,000

After harvesting, you can reinvest in a similar fund or ETF, ensuring that your market exposure remains unchanged.

This makes tax harvesting a tax-efficient portfolio adjustment, not a market timing strategy.

Why It Matters Before 31 March

Tax harvesting must be completed before the financial year ends because:

• Capital gains tax is calculated FY-wise

• Losses must be realised to be set off

• Unused losses can be carried forward only if reported

• Market volatility near year-end creates harvesting opportunities

Missing the March deadline means losing the opportunity to optimise taxes for the current year.

Tax Harvesting Rules in India (2026)

Understanding taxation is crucial before implementing the strategy.

Equity (Stocks, Equity Mutual Funds, ETFs)

Short-Term Capital Gain (STCG)

Holding period: Less than 12 months

Tax rate: 20%

Long-Term Capital Gain (LTCG)

Holding period: More than 12 months

Tax rate: 12.5% above ₹1.25 lakh exemption

Loss Set-Off Rules

• Short-term capital loss (STCL) can offset both STCG and LTCG

• Long-term capital loss (LTCL) can offset only LTCG

• Unused losses can be carried forward for 8 years

This makes short-term loss particularly valuable for active investors.

Tax Harvesting Using Mutual Funds

Many investors believe tax harvesting applies only to stocks, but mutual funds are often easier to use.

Benefits:

• Diversified risk

• Simpler execution

• Behaviourally easier

• Ideal for SIP investors

Example:

Sell → Underperforming Flexicap Fund (loss)

Buy → Another Flexicap or Nifty ETF

This ensures:

• Loss realised for tax benefit

• Equity allocation maintained

ETF vs Mutual Fund Harvesting

ETF Advantages

• Intraday liquidity

• Precise execution

• Tactical switching possible

• Lower tracking error

Mutual Fund Advantages

• Suitable for long-term investors

• Easier for SIP portfolios

• Less behavioural stress

Best approach:

Use both strategically.

Real Example: Tax Harvesting Impact

Assume an investor has:

Realised LTCG = ₹3,00,000

LTCG exemption = ₹1,25,000

Taxable gain:

₹1,75,000

Tax payable:

₹21,875

Now suppose the investor harvests:

Mutual fund loss = ₹1,00,000

Revised taxable gain:

₹75,000

Tax payable:

₹9,375

Tax saved:

₹12,500

If this amount remains invested at 12% for 15 years:

Future value ≈ ₹68,000

This shows how tax harvesting improves long-term wealth creation.

Tax Loss Harvesting Calculator Framework

You can use this simple step-by-step approach.

Step 1: Calculate realised gains

STCG + LTCG during the financial year.

Step 2: Apply LTCG exemption

Deduct ₹1.25 lakh from long-term gains.

Step 3: Identify unrealised losses

From stocks, mutual funds, ETFs.

Step 4: Apply set-off rules

Adjust short-term losses first.

Step 5: Calculate tax saved

Tax saved = Loss harvested × applicable tax rate.

Long-Term Impact Formula

Future value of tax saved:

FV = Tax Saved × (1 + return)^years

This demonstrates the compounding power of tax efficiency.

Quick Tax Harvesting Impact Table

| Harvested Loss | Tax Saved (10% assumed) | Value After 15 Years (12%) |

|---|---|---|

| ₹50,000 | ₹5,000 | ₹27,000 |

| ₹1,00,000 | ₹10,000 | ₹54,000 |

| ₹2,00,000 | ₹20,000 | ₹1,08,000 |

| ₹3,00,000 | ₹30,000 | ₹1,62,000 |

Active investors in higher tax brackets benefit even more.

Practical Switching Ideas (Mutual Funds + ETFs)

The key principle:

Maintain portfolio exposure while realising loss.

Large Cap Allocation

Switch:

• Nifty ETF → Nifty Next 50 ETF

• Large cap mutual fund → Index fund

Midcap Allocation

Switch:

• Midcap fund → Flexicap fund

• Midcap ETF → Broad market ETF

Flexicap Allocation

Switch:

• One AMC flexicap → another AMC flexicap

• Flexicap → mix of large + mid ETFs

Sector Funds

If sector underperformed:

• IT / Pharma fund → Broad market fund

Avoid concentrated risk.

Debt Fund Tax Harvesting (Important After 2023 Rule Change)

Debt mutual funds are now taxed at slab rates.

This makes harvesting losses in:

• Long duration funds

• Gilt funds

• Credit funds

particularly valuable.

Switch to:

• Short duration

• Corporate bond

• Money market funds

This improves tax efficiency without exiting debt allocation.

You can check overlap in mutual funds using online tools like Fundoo!

SIP Investors: Hidden Opportunity

SIP portfolios contain multiple purchase lots.

Some units may be in loss even if the overall fund is positive.

Strategy:

• Redeem only loss units

• Reinvest immediately

This enhances tax efficiency without disturbing long-term investment discipline.

When Not to Do Tax Harvesting

Avoid harvesting if:

• You hold a high-conviction long-term compounder

• Exit loads are significant

• Loss is temporary market noise

• Portfolio allocation gets distorted

Tax optimisation should never compromise investment quality.

Final Thought: Tax Efficiency is a Compounding Multiplier

Investment success depends on:

• Asset allocation

• Behaviour

• Costs

• Taxes

Most investors optimise the first three.

Few optimise taxes.

But over decades:

Tax harvesting can increase wealth by 15–25%.

As 31 March 2026 approaches, reviewing your portfolio for tax harvesting may be one of the most impactful financial decisions you make this year.

Because in investing:

Returns earned matter — but returns kept after tax matter more.

Check out the Alternative Investments list below

In the “Real Example: Tax Harvesting Impact” provided wouldn’t tax payable be Rs.7,500 (10% of Rs.75,000)?

Hi Mahadevan,

LTCG is applicable only over INR 100,000 gains in a year.

Sorry, but isn’t it 12.% on gains above 1,25,000?

So, it should be 12.5% of 75,000 (3,00,000-1,00,000-1,25,000) which is 9,375

Please see this:

https://www.bajajfinserv.in/investments/long-term-capital-gain-tax-on-shares

You are correct, I have made the changes in the article